Featured

Table of Contents

Handling Interest Costs in Debt Consolidation Near Throughout 2026

The financial environment of 2026 presents particular difficulties for families attempting to stabilize monthly budgets against consistent rate of interest. While inflation has actually stabilized in some sectors, the cost of carrying consumer debt remains a substantial drain on individual wealth. Lots of homeowners in Debt Consolidation Near discover that standard techniques of debt repayment are no longer sufficient to keep up with compounding interest. Effectively browsing this year requires a strategic focus on the overall cost of borrowing rather than simply the monthly payment quantity.

Among the most frequent mistakes made by customers is relying entirely on minimum payments. In 2026, charge card rate of interest have reached levels where a minimum payment hardly covers the regular monthly interest accrual, leaving the primary balance essentially unblemished. This develops a cycle where the financial obligation continues for years. Shifting the focus towards reducing the interest rate (APR) is the most effective way to shorten the repayment period. People looking for Debt Consolidation frequently discover that financial obligation management programs provide the necessary structure to break this cycle by negotiating directly with financial institutions for lower rates.

The Threat of High-Interest Combination Loans in the Regional Market

As debt levels rise, 2026 has seen a surge in predatory loaning masquerading as relief. High-interest consolidation loans are a typical risk. These products promise a single month-to-month payment, however the underlying interest rate may be higher than the typical rate of the initial debts. If a consumer utilizes a loan to pay off credit cards but does not resolve the hidden spending habits, they typically end up with a big loan balance plus new credit card financial obligation within a year.

Not-for-profit credit therapy provides a different path. Organizations like APFSC offer a debt management program that combines payments without the need for a new high-interest loan. By overcoming a 501(c)(3) not-for-profit, people can gain from developed relationships with national lenders. These partnerships enable the agency to work out considerable rates of interest decreases. Local Debt Consolidation Experts provides a path toward financial stability by guaranteeing every dollar paid goes even more towards lowering the real debt balance.

Geographic Resources and Neighborhood Assistance in the United States

Financial healing is typically more effective when localized resources are involved. In 2026, the network of independent affiliates and community groups across various states has actually become a foundation for education. These groups provide more than just financial obligation relief; they provide financial literacy that helps prevent future debt build-up. Because APFSC is a Department of Justice-approved firm, the counseling supplied fulfills rigorous federal standards for quality and openness.

Real estate remains another considerable consider the 2026 financial obligation formula. High home loan rates and increasing rents in Debt Consolidation Near have pushed many to utilize charge card for fundamental necessities. Accessing HUD-approved real estate counseling through a nonprofit can help citizens manage their real estate expenses while simultaneously dealing with customer debt. Households often search for Debt Consolidation in Coral Springs to acquire a clearer understanding of how their rent or home mortgage engages with their overall debt-to-income ratio.

Avoiding Typical Errors in 2026 Credit Management

Another pitfall to avoid this year is the temptation to stop communicating with creditors. When payments are missed, rate of interest typically surge to charge levels, which can go beyond 30 percent in 2026. This makes an already challenging situation nearly difficult. Expert credit counseling serves as an intermediary, opening lines of interaction that an individual might find challenging. This process helps protect credit rating from the extreme damage triggered by overall default or late payments.

Education is the best defense against the rising costs of debt. The following techniques are necessary for 2026:

- Examining all charge card declarations to recognize the present APR on each account.

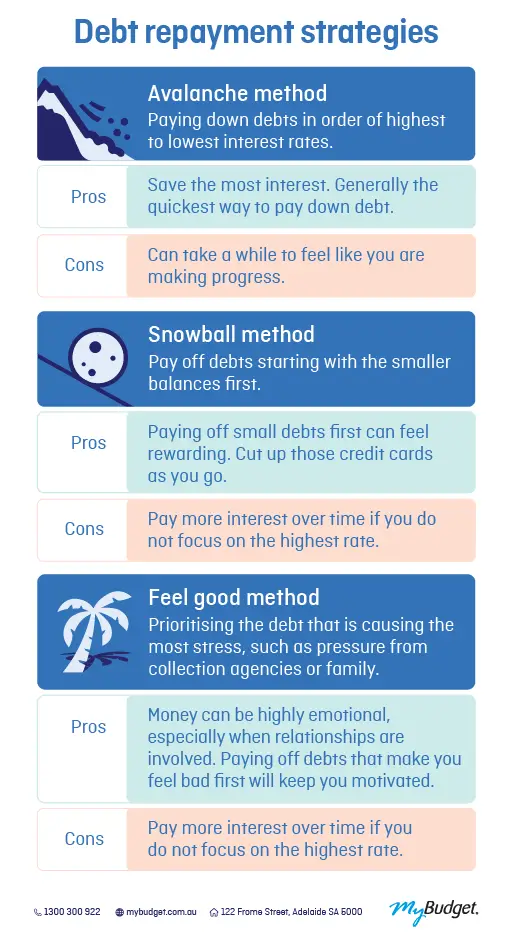

- Focusing on the payment of accounts with the greatest rate of interest, frequently called the avalanche method.

- Looking for not-for-profit help rather than for-profit debt settlement business that might charge high charges.

- Utilizing pre-bankruptcy therapy as a diagnostic tool even if insolvency is not the designated goal.

Nonprofit agencies are needed to act in the finest interest of the consumer. This consists of offering free preliminary credit counseling sessions where a licensed therapist reviews the individual's whole monetary photo. In Debt Consolidation Near, these sessions are typically the initial step in recognizing whether a debt management program or a various financial strategy is the most appropriate choice. By 2026, the complexity of monetary items has actually made this expert oversight more vital than ever.

Long-Term Stability Through Financial Literacy

Reducing the overall interest paid is not just about the numbers on a screen; it is about recovering future earnings. Every dollar conserved on interest in 2026 is a dollar that can be rerouted toward emergency situation cost savings or retirement accounts. The financial obligation management programs provided by agencies like APFSC are created to be short-term interventions that cause irreversible changes in monetary habits. Through co-branded partner programs and local monetary organizations, these services reach varied communities in every corner of the country.

The goal of handling financial obligation in 2026 needs to be the total elimination of high-interest customer liabilities. While the procedure requires discipline and a structured strategy, the results are quantifiable. Decreasing rate of interest from 25 percent to under 10 percent through a negotiated program can conserve a family countless dollars over a couple of short years. Avoiding the risks of minimum payments and high-fee loans permits citizens in any region to move toward a more secure monetary future without the weight of uncontrollable interest costs.

By concentrating on confirmed, nonprofit resources, consumers can browse the economic challenges of 2026 with confidence. Whether through pre-discharge debtor education or standard credit counseling, the objective remains the same: a sustainable and debt-free life. Doing something about it early in the year guarantees that interest charges do not continue to compound, making the eventual goal of debt freedom easier to reach.

{kind=link}

Latest Posts

The Best Ways to Pay Down Cards in Your Area

The Benefits of Lower Interest Rates in 2026

The Financial Effect of Refinancing Financial Obligation in 2026